The government and central bank are calling for "wage restraint". But with workers facing surging housing costs, what are employers supposed to do?

- The Office for Budget Responsibility warned UK national debt could exceed 300 per cent of GDP by 2070.

- Disney’s board voted to extend Bob Iger’s tenure as CEO until 2026 (more below).

- Rishi Sunak announced pay rises for public sector workers of between 5 and 7 per cent.

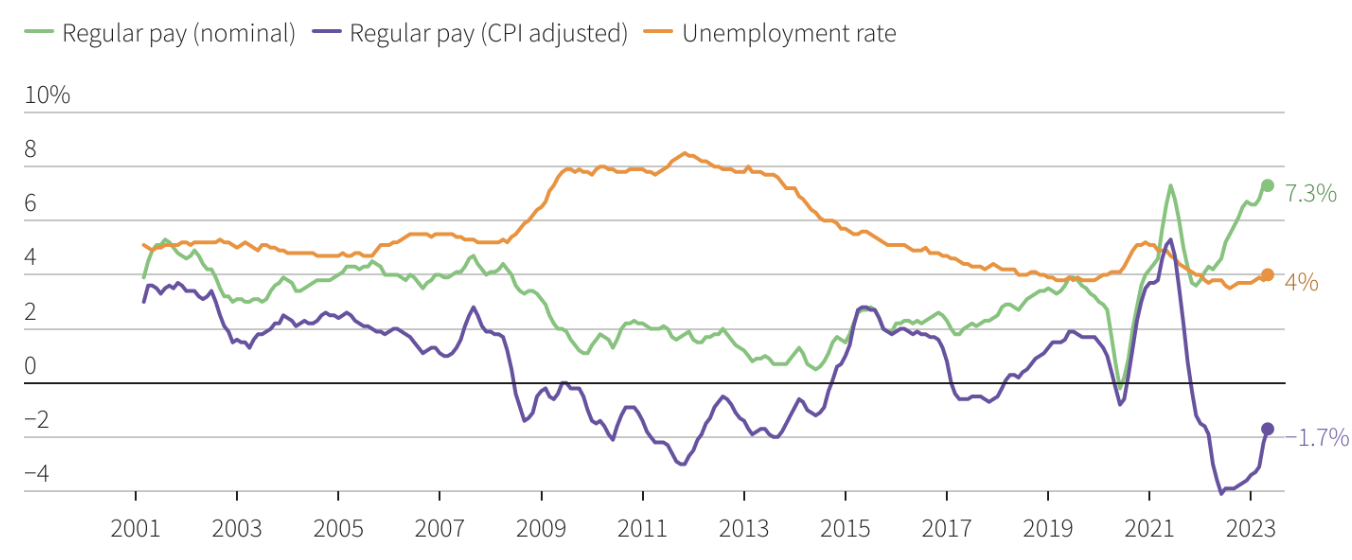

On Monday the Chancellor and the Governor of the Bank of England made a united plea to British employers to exercise “wage restraint” after a key measure showed wages rose at a joint record rate over the past three months.

So what? It’s wishful thinking. The rise in inflation to a 40-year high is expected to reduce real household disposable incomes by 2.2 per cent – the biggest squeeze since the 1950s. Ballooning housing costs for both renters and mortgage holders are becoming an acute source of pain. Employers have limited ways to help their employees besides pay increases – as the government itself has shown by agreeing to raise public sector pay by 6.5 per cent.

By the numbers:

10.4 per cent – increase in average monthly rent for a new tenancy in the UK compared to last year.

£220 – increase in monthly payments faced by a typical mortgage holder coming off a fixed-rate deal in the next six months.

8 per cent – of post-tax income UK households are expected to spend on mortgage payments by 2026, up from 5.5 per cent now.

44 per cent – people who say they are “struggling” or “falling behind” on housing costs, according to YouGov.

-1.2 per cent – decline in real-terms total pay between March and May, a rate last seen post-financial crash.

The UK is now the mirror-image of a low-interest economy. Inflation, savings and interest rates are all high, while unemployment is relatively low. Overcoming the impact of Brexit, which in effect made Britain poorer by raising the cost of imported goods, can only be solved in the long-term by boosting domestic productivity.

For now, Jeremy Hunt and Andrew Bailey face the unenviable task of threading the needle between containing inflation and avoiding recession. Either way, the pain won’t be spread equally:

- Sector. Data from the Office for National Statistics (ONS) shows strong wage increases for white-collar workers in science and finance that are above or in line with inflation. The same can’t be said for those in hospitality and retail, who are more likely to be taking a real-terms pay cut. “One of the problems we’ve got is there is real variation in wage growth across sectors at the moment, and therefore you’ve got growing inequality in the labour market,” says Alfie Stirling, chief economist at the Joseph Rowntree Foundation.

- Age. There is a swathe of the economy who aren’t negatively impacted by rising rates: 72 per cent of over 65s own property outright, compared to 90 per cent of people under 35 who live in mortgaged or rented accommodation. The IFS says that 40 to 50 per cent of people born during or after the 1980s are private renters.

- Living situation. Renters are faring disproportionately badly. Around seven in 10 low-income private and social renters have gone without essentials such as basic toiletries or prescriptions in the last six months, according to the Joseph Rowntree Foundation. The effect is magnified in London, where over a quarter of low-income renters are currently in arrears.

What else can employers do? Many businesses are already offering financial advice and alternative forms of support to employees. They can also make efforts to mitigate income uncertainty for shift and part-time workers, allowing them to better plan for changes in their housing costs.

“Sustained action is very patchy,” says Ben Harrison, director of the Work Foundation at Lancaster University. “There’s a lot of ad hoc support, but there’s a gap in terms of engagement to really understand how different workers are coping with increases in mortgages or other core expenses like food.”

And policymakers? “It’s really incumbent on the government to act preemptively to offset the worst impacts distributionally,” says Stirling. This could be achieved by:

- beefing up support for mortgage interest payments. Currently this takes the form of a loan which only covers 2.65 per cent of interest and must be paid back.

- unfreezing Local Housing Allowance to realign it with soaring rents.

- re-growing the social rental sector by providing it with enough capital to buy housing stock from buy-to-let landlords now looking to sell.

Hunt cannot afford to sit back while interest rates begin to hit. Repossessions are already beginning to tick up. Recession in the 1990s occurred after rates climbed above 7 per cent and mortgages became widely unaffordable. Average two-year fixed rates are now at 6.6. British “restraint” isn’t going to cut it.